Ferrous Fades, Non-Ferrous Flares.

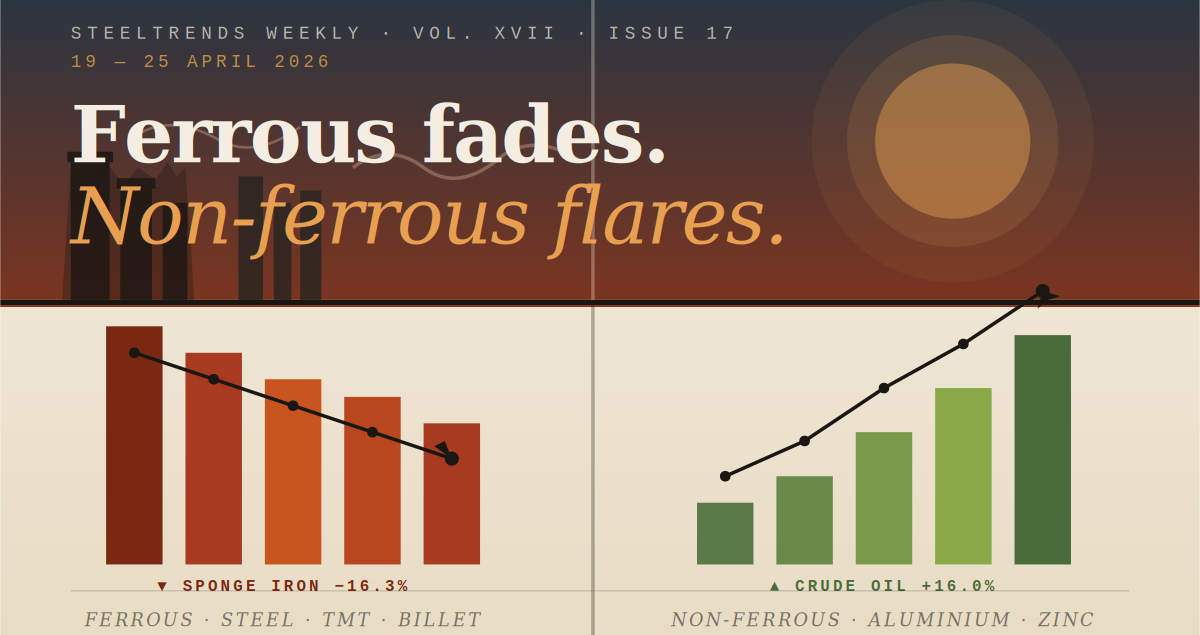

A week of two markets: India's TMT, billet, and sponge iron complex slipped into a broad downtrend even as aluminium, zinc, and copper rallied on Strait of Hormuz disruption. The result is a near-perfect bifurcation — 13 bearish products to two bullish — that procurement managers cannot afford to misread.

The Tale of Two Markets

Why India's steel and metal complex split clean down the middle this week.

If you traded only one product this week, the headline number on your screen lied to you. The Indian steel and metal market did not move in one direction — it tore in two. On one side, the entire ferrous chain from sponge iron to finished TMT ground lower, weighed down by a quiet pre-monsoon demand pause and softening raw material costs. On the other, base metals — aluminium, zinc, copper, and the broader non-ferrous complex — pushed higher, dragged up by a supply shock unfolding nearly 3,000 kilometres west of Mumbai, in the Strait of Hormuz.

The split was clean and unambiguous. Out of fifteen tracked product categories, thirteen finished the week in a downtrend, two finished higher, and zero closed sideways. Yet the magnitude of the two upside moves — concentrated almost entirely in the Metal category — was loud enough to drown out half the bearish signals in any single-line summary.

For procurement managers, fabricators, and traders alike, the implication is operational. If you buy steel, this week was a buyer's market. If you consume aluminium or copper, you missed your window — and probably won't get it back soon.

The Ferrous Slump: Demand Pauses, Mills Adjust

A textbook pre-monsoon cooling, with sponge iron leading the descent.

The clearest signal of weakness came from sponge iron, where the category average fell −16.3% over the week, the steepest move in any product group. Two reporting hubs (Raipur and Pellet Mandi Gobindgarh) showed zero closing values, which mathematically punished the average, but even setting those outliers aside, the trend across reporting cities is unmistakable. Bellary fell 1.8% to ₹27,800/MT. Durgapur dropped 1.7%. Mandi Gobindgarh slid 1.8%.

This corroborates industry reporting from mid-April: sponge iron prices in Bellary correcting by roughly ₹1,100/MT week-on-week, attributed to softening non-coking coal costs and reduced buying interest from induction-furnace operators. When non-coking coal eases and DRI economics weaken at the margin, induction furnaces have less reason to chase sponge iron aggressively — and prices give way.

Downstream, the bearish signal carried into billets, ingots, and TMT bars. Company TMT dropped 1.6% on the week, with a wide regional spread: secondary brands like Jai Kapish in Durgapur and Kolkata fell 3.3%, Mumbai's Metro brand shed 3.6%, and Jaipur Jindal lost 3.0%. The TMT 12mm category mirrored this, posting a 1.2% weekly decline with virtually every major hub showing red.

Yet absolute price levels remain, by any historical measure, structurally elevated. Lucknow's primary-grade brands held at ₹60,000/MT despite the weekly slip — consistent with industry data showing primary TMT continues to trade firm above ₹60,000/MT through April, supported by elevated coking coal costs and government infrastructure offtake. This week's softness sits inside an April that, on balance, was supportive for primary steel.

The Hormuz Squeeze: Why Aluminium Defied Steel

A geopolitical chokepoint half a world away rewrote India's base-metal pricing.

While ferrous prices drifted, base metals refused to participate in the slump. The Metal category — spanning aluminium, copper, zinc, lead, nickel, plus precious metals and battery scrap — closed the week up +0.9%, but that average is misleading: the gainers ran much harder. Aluminium ingot rose 2.7%. Aluminium purja added 3.1%. Aluminium section, utensil, and wire scrap all pushed up between 1.8% and 2.2%. Zinc gained 2.6%. Copper added 1.6%. And crude oil — included as a freight and energy proxy — exploded +16.0% on the week, the single largest move in the entire dataset.

The driver was almost entirely external to India: the continuing disruption of the Strait of Hormuz, the chokepoint through which roughly 9% of global primary aluminium output sails. London Metal Exchange aluminium traded near a four-year high through April 22, with confirmed damage to refining and smelting facilities in the UAE and Bahrain. Emirates Global Aluminium, the region's largest producer, said it could take at least a year to fully restore output — effectively converting a logistics shock into a multi-quarter supply problem.

India is a net consumer at the margin for many of these metals, and our domestic prices track LME with a short lag. When the LME runs, Mumbai, Delhi, and Ahmedabad scrap dealers run too — and that is exactly what the data captured.

Where the Pain Concentrated

A look at the cities and brands that took the worst of the week.

The bearish move was not evenly distributed. Eastern India bore the brunt, particularly the Durgapur–Kolkata–Ramgarh belt, where induction-furnace clusters depend heavily on local sponge iron pricing for cost discipline. Ramgarh billet dropped 3.9% to ₹41,800/MT. Ramgarh ingot fell 4.0%. Durgapur's Jai Kapish brand fell 3.3% across both Durgapur and Kolkata yards. Goa, often a laggard during regional softness, saw its billet category drop 3.3% and TMT 12mm drop 1.8%.

Conversely, the Western billet market actually firmed in pockets. Alang led with a +1.8% weekly gain to ₹45,800/MT, Bhavnagar added 1.1%, and Ahmedabad was up 0.4% — a divergence likely tied to ship-breaking yard activity at Alang feeding shorter-cycle billet remelt demand. Where ship scrap is moving, billet stays bid. That is a useful local signal even when the national tape looks weak.

Top Movers This Week

The names that did the heaviest lifting — in both directions.

| Metal | Crude | 7,616 | 8,835 | +16.0% | Metal | Aluminium Purja | 286 | 295 | +3.1% | Metal | Aluminium | 364 | 374 | +2.8% | Metal | Aluminium Ingot | 368 | 378 | +2.7% | Metal | Zinc | 340 | 349 | +2.6% | Structural | Gobindgarh Patra | 49,300 | 47,300 | −4.1% | Ingot | Ramgarh | 42,500 | 40,800 | −4.0% | Billet | Ramgarh | 43,500 | 41,800 | −3.9% | TMT | Mumbai (Metro) | 53,100 | 51,200 | −3.6% | Ingot | Goa | 44,600 | 43,100 | −3.4% | Billet | Goa | 45,000 | 43,500 | −3.3% |

The Week Ahead: Three Things Worth Watching

Catalysts, not predictions, for the week of 27 April – 3 May.

The Bottom Line for Buyers

Translating the data into action.

For procurement managers with project commitments in the next 30–45 days, this week looks like an opportunity in steel and a missed window in non-ferrous. Locking in secondary TMT at the current ₹47,000–53,500/MT band, particularly in Eastern hubs where the discount has widened, is defensible. Primary TMT remains harder to time given mill discipline above ₹60,000/MT. Billet buyers should position for a Raipur-led recovery if Alang's strength carries through to next week.

For aluminium and zinc consumers, the call is harder. The Hormuz overhang is structural until refining capacity returns, and chasing prices that have already moved 2.5%+ in a week is rarely a winning trade. Better to hedge forward exposure, accept higher near-term landed costs, and wait for either a geopolitical resolution or a demand-side cooling — whichever arrives first.

The single piece of advice that holds across both halves of the market this week is the oldest one: don't trade the average. Trade the spread. When fifteen product categories split this cleanly, the right move is rarely the one the headline number suggests.